Credit Card Points vs. Cash Back: Which Rewards System Maximizes Your Return

Published on May 3, 2025

Hey friends! I want you to imagine this scenario with me: You’re standing at the checkout line watching the cashier scan your items, and the total keeps climbing. $57.82… $82.46… $124.31. Your heart starts to race a little—but then you remember you’ve got your rewards credit card, and a small smile crosses your face. Those purchases are actually working for you now, not just draining your bank account!

That’s the beauty of credit card rewards. When used wisely (and I can’t stress the “wisely” part enough), they can actually put money back in your pocket or fund amazing experiences. But here’s where things get tricky—should you choose cash back or points? This question leaves so many people confused and potentially missing out on hundreds or even thousands of dollars in value each year.

Y’all, I’ve been there! I used to think all rewards were pretty much the same. Boy, was I wrong! After diving deep into the research and applying these strategies in my own life, I’ve discovered there’s a whole world of difference between these two reward systems. And today, I’m going to break it all down for you in plain English—no fancy financial jargon required!

The big decision: Cash back simplicity or points flexibility?

Table of Contents

- Understanding Rewards Systems: The Basics You Need to Know

- Which Type of Rewards System Is Right for YOU?

- Cash Back Cards: The Deep Dive

- Points and Miles: Unlocking Exceptional Value

- Universal Strategies: Maximizing Any Rewards System

- Making Your Choice: Personal Assessment Questions

- Beyond the Rewards: The Full Financial Picture

- Finding Your Perfect Rewards Match: Final Thoughts

- Frequently Asked Questions

Understanding Rewards Systems: The Basics You Need to Know

Before we dive into which system is best, let’s make sure we’re all on the same page about how these rewards actually work. It’s like learning the rules of a game before deciding which strategy to use!

Cash Back: The Straightforward Approach

Cash back is exactly what it sounds like—you get actual money back on your purchases. Simple, right? According to recent surveys, about 58% of cardholders prefer cash back cards over other reward options. And I totally get why! There’s something so satisfying about seeing real dollars coming back to you.

Most cash back cards work in one of three ways:

- Flat-rate cards: You earn the same percentage (usually 1-2%) on every purchase you make. Super simple!

- Tiered category cards: You earn higher percentages (often 3-5%) on specific categories like groceries or gas, and a lower rate (usually 1%) on everything else.

- Rotating category cards: You earn elevated rewards (often 5%) on categories that change quarterly, like restaurants in the summer or online shopping during the holidays.

The beauty of cash back is there’s no guesswork about value. If you earn 2% cash back on a $100 purchase, that’s $2 back in your pocket. Period. No calculations, no fluctuations in value.

Points and Miles: The Flexible Approach

Points and miles are a bit more complex, which is why they can intimidate folks at first. Instead of earning a percentage back, you earn a certain number of points per dollar spent. These points can then be redeemed for various things—travel, gift cards, merchandise, or sometimes even cash back (though usually at a lower value).

According to industry data, around 31% of cardholders currently use cards that offer points or miles rewards systems. Why fewer than cash back? Well, they require a bit more work and understanding, but as you’ll see, that extra effort can sometimes lead to significantly higher returns!

What makes points interesting is that their value can vary dramatically depending on how you redeem them. For example, 10,000 points might be worth:

- $100 when redeemed for travel through the card’s portal

- $125 or more when transferred to airline or hotel partners

- Only $60-$70 when redeemed for merchandise

- $100 as a statement credit

This variability is both a blessing and a curse. On one hand, if you’re strategic, you can extract tremendous value from your points. On the other hand, it’s easy to redeem them inefficiently and leave value on the table.

Which Type of Rewards System Is Right for YOU?

I’m a firm believer that personal finance is PERSONAL! What works amazingly for your neighbor might be completely wrong for you. So instead of giving a one-size-fits-all answer, let’s look at different types of spenders and which reward system might serve them best.

Making the right choice can lead to greater financial freedom and satisfaction

Cash Back May Be Perfect For You If:

- You’re a simplicity lover: You want rewards without having to think too much about redemption strategies.

- You’re budget-conscious: You want to directly reduce your expenses with predictable returns.

- You rarely travel: Since many points systems offer the best value for travel redemptions, if you don’t travel often, you might not benefit as much.

- You’re a moderate spender: If your monthly credit card spending is modest, the potential gains from complex points strategies might not justify the effort.

- You prefer immediate gratification: You’d rather see rewards credited back to your account regularly than save up for big redemptions.

When I was first getting my finances in order, cash back was my go-to. It was easy to understand, simple to redeem, and helped me stay focused on my budgeting goals. For many people just starting out with rewards cards, this simplicity is exactly what they need!

Points and Miles May Be Better For You If:

- You’re a frequent traveler: If you love to travel or have to for work, points can offer exceptional value for flights and hotels.

- You’re a big spender: Higher monthly spending means accumulating points faster, making premium redemptions more accessible.

- You enjoy optimizing: If you get a thrill from finding the perfect redemption and maximizing value, points systems reward that effort.

- You plan big purchases: Points are great for saving toward specific goals like a dream vacation or premium flight experience.

- You don’t mind annual fees: Many of the best points cards come with annual fees, but their benefits can far outweigh the cost for the right user.

My husband and I discovered the value of points systems when planning our anniversary trip a few years back. By strategically using points, we were able to book business class flights that would have cost thousands of dollars—all from our regular spending throughout the year! Talk about a relationship upgrade!

Cash Back Cards: The Deep Dive

Let’s be real—there’s something wonderfully satisfying about seeing actual cash back in your account. No complicated redemptions, no wondering if you’re getting the best value. Just cold, hard cash (well, electronic, but you know what I mean!).

Understanding the Numbers: What’s a Good Cash Back Rate?

The average cash back rate across all cards is around 1.17%, according to recent industry data. But that doesn’t mean you should settle for average! Here’s how different cash back rates stack up:

| Cash Back Rate | Category | How Common | Annual Return on $15,000 Spend |

|---|---|---|---|

| 1% | Base rate on most cards | Very common | $150 |

| 1.5% | Flat rate on mid-tier cards | Common | $225 |

| 2% | Excellent flat rate | Less common | $300 |

| 3-5% | Bonus categories | Common but limited to specific purchases | $450-$750 (if all spending qualified) |

One Reddit user I came across shared that they managed to achieve an amazing 4% average cash back rate by strategically juggling 8 different credit cards! That’s dedication, y’all! But for most of us, a simpler approach with 2-3 well-chosen cards can still yield an impressive 3% average return.

Pros of Cash Back

- Simple to understand and use

- Fixed, predictable value

- Flexible—can be used for anything

- Many no-annual-fee options

- Immediate gratification with statement credits

Cons of Cash Back

- Generally lower potential maximum value

- Fewer premium perks and benefits

- Smaller welcome bonuses compared to points cards

- Limited opportunity for outsized value

- May require multiple cards for optimal returns

Maximizing Your Cash Back Strategy

Y’all know I love practical advice, so here are my top tips for getting the most out of cash back cards:

- Start with a strong base card. Look for a card offering at least 1.5% or 2% on everything. This ensures you’re never earning less than a decent rate.

- Add strategic category cards. Once you have your base card, add 1-2 cards that offer high rewards (3-5%) in categories where you spend the most, like groceries or gas.

- Don’t overlook rotating category cards. Cards that offer 5% in rotating categories can supercharge your returns if you’re willing to keep track of the quarterly changes.

- Stack with shopping portals. Many card issuers have shopping portals where you can earn additional cash back on top of your regular card rewards. This is like double-dipping!

- Set up automatic redemptions. Some cash back stays in your rewards account until you manually redeem it. Don’t let it sit there! Set up automatic redemptions so you’re actually using what you earn.

One thing I love about cash back is how it aligns with good budgeting habits. When you get cash back, you can immediately apply it to your budget—either by reducing expenses or adding to your savings. It’s a direct boost to your financial goals!

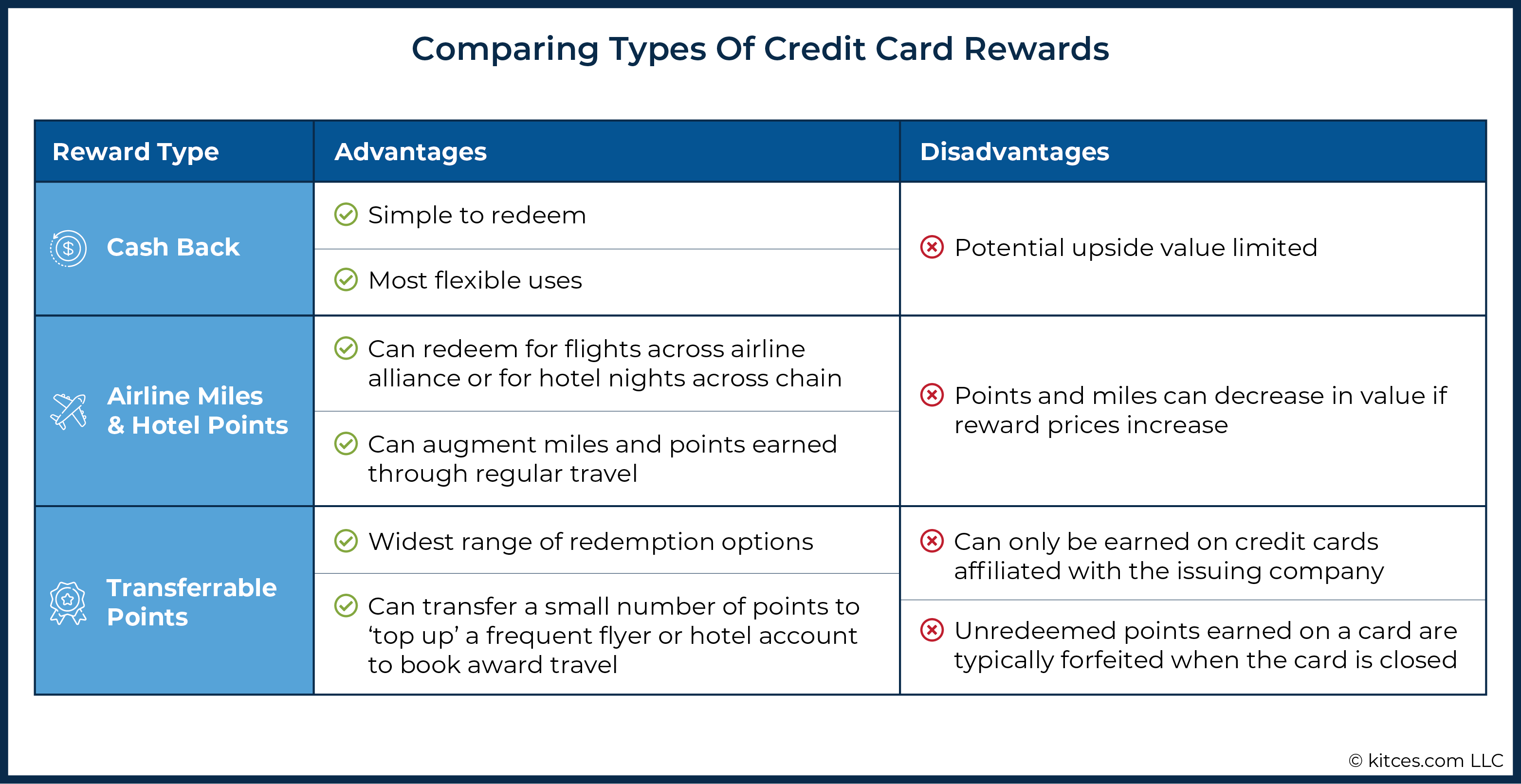

Points and Miles: Unlocking Exceptional Value

Now let’s talk about points and miles—the reward system that can feel like a whole new language at first but can offer tremendous value if you’re willing to learn a few key concepts!

The different types of credit card rewards systems and their components

Understanding Point Valuation: Not All Points Are Created Equal

This is where things get interesting! Unlike cash back, where a penny is always worth a penny, the value of points can vary dramatically depending on which program they’re in and how you redeem them.

Here’s an example of how points values can differ across major programs:

| Rewards Program | Base Redemption Value | Potential Transfer Value | Notes |

|---|---|---|---|

| Chase Ultimate Rewards | 1-1.5 cents per point | 1.5-2+ cents per point | Value depends on which Chase card you have |

| American Express Membership Rewards | 0.6-1 cent per point | 1.5-2+ cents per point | Best value through airline transfers |

| Capital One Miles | 1 cent per point | 1.2-1.8 cents per point | Growing transfer partner list |

| Airline Miles (varies by program) | 0.7-1.2 cents per mile | Up to 5+ cents per mile | Highest values usually for international premium cabins |

| Hotel Points (varies by program) | 0.4-0.7 cents per point | Up to 2+ cents per point | Value varies widely by property and season |

Did you catch that? The same point can be worth FIVE TIMES as much depending on how you use it! That’s why people get so excited about points—there’s potential for outsized value that cash back simply can’t match.

Transferable Points: The Crown Jewel of Rewards

The most valuable points are typically transferable points—those that can be moved to multiple airline and hotel partners. Think of them as the Swiss Army knife of rewards! They give you incredible flexibility to find the best value for your specific needs.

For example, let’s say you want to fly to Europe. With cash back, you might save up $800 for an economy ticket. But with transferable points, you could potentially:

- Transfer 60,000 points to an airline partner for a business class seat worth $2,500+

- Book through your card’s travel portal for a standard economy ticket

- Hold onto your points if prices are high and use them when there’s better value

This flexibility means you can often get 2-3 cents per point in value, far exceeding the 1-2% return of most cash back cards.

Pros of Points & Miles

- Potential for outsized value (2-5+ cents per point)

- Better for luxury travel experiences

- Typically larger welcome bonuses

- More premium card benefits (lounge access, travel credits)

- Flexibility through transfer partners

Cons of Points & Miles

- More complex to understand and maximize

- Values can change without notice (devaluations)

- Often require more planning for optimal use

- Many premium cards have substantial annual fees

- May need to be flexible with travel dates/destinations

Maximizing Your Points Strategy

If you’re intrigued by the potential of points, here are my top strategies for making the most of them:

- Focus on welcome bonuses. Points cards often offer huge initial bonuses—sometimes 100,000 points or more! These can jump-start your rewards journey.

- Understand transfer partners. Research which airlines and hotels partner with your credit card program and learn the sweet spots for redemptions.

- Avoid low-value redemptions. Using points for merchandise or gift cards typically gives poor value (often below 1 cent per point). Save your points for travel!

- Look for transfer bonuses. Card issuers occasionally offer bonuses (like “transfer 1,000 points, get 1,250 miles”), which can boost your value even further.

- Consider annual fees as investments. A $95 annual fee might seem steep, but if it helps you earn points worth $1,000+, that’s a fantastic return!

I know a family that used a strategic approach to points collecting and managed to take their family of four to Disney—flights, hotel, AND park tickets—entirely on points. What would have cost them over $5,000 in cash cost $0 out of pocket (beyond the card’s annual fee). Now THAT’S what I call smart money management!

Universal Strategies: Maximizing Any Rewards System

Whether you choose cash back or points, some strategies work well for BOTH systems. Let’s look at how to supercharge your rewards regardless of which path you choose!

Smart reward strategies can lead to real financial wins worth celebrating!

Strategic Card Combinations

One of the most powerful approaches is to use multiple cards strategically. According to a J.D. Power survey, cardholders who use multiple rewards cards strategically earn up to 40% more rewards than those who rely on a single card!

Here’s a simple but effective three-card strategy:

- A premium card with strong benefits for your highest-value category (like travel or dining)

- A category specialist card that excels in another key spending area (like groceries or gas)

- A flat-rate card for everything else that doesn’t fall into bonus categories

This approach ensures you’re maximizing every dollar without needing a wallet full of cards.

Welcome Bonuses: The Fast Track to Rewards

Y’all, I cannot emphasize this enough—welcome bonuses are often the quickest way to earn a large chunk of rewards! It’s not uncommon to see offers worth $500-$1,000+ in value just for meeting a minimum spending requirement.

But here’s my important caution: Never increase your spending just to hit a bonus. That’s a slippery slope that can lead to debt, which undermines the whole purpose of rewards! Only pursue welcome bonuses if the spending requirement aligns with what you’d normally spend anyway.

Timing Your Applications

Credit card companies often increase their welcome bonus offers seasonally. For example, travel cards frequently offer better bonuses in late spring as people start planning summer vacations. If you’re eyeing a particular card, it might pay to watch for a few months to catch a better offer.

Also be aware of rules like Chase’s “5/24 rule” (you likely won’t be approved if you’ve opened 5 or more cards in the past 24 months) or Amex’s “once-per-lifetime” bonus policy. These can impact your application strategy.

Maximizing Category Bonuses

Take full advantage of bonus categories! Some strategies to consider:

- Set calendar reminders when rotating categories change

- Update the default card on your online shopping accounts when beneficial

- Consider buying gift cards at stores with bonus earning (like grocery stores) to use later at stores without bonuses

- Add authorized users strategically to help meet spending thresholds that unlock higher rewards

Making Your Choice: Personal Assessment Questions

At this point, you might be leaning toward one system or the other. Let’s solidify your decision with some self-reflection questions:

Ask Yourself These Questions:

- How do I feel about planning and research?

If you enjoy optimization and don’t mind spending time learning about redemption options, points may be more rewarding. If you prefer simplicity, cash back is likely better. - How much do I spend monthly on credit cards?

Higher spenders (over $2,000 monthly) often benefit more from points systems due to faster accumulation and better premium card perks. - Do I travel regularly or aspire to?

If travel is a priority, points typically offer substantially better value. If not, the higher potential value of points may be irrelevant to you. - Am I comfortable with annual fees?

Premium rewards often come with premium annual fees. Are you willing to pay upfront for better benefits and earning potential? - How disciplined am I with credit cards?

Be honest with yourself! Rewards cards should enhance your financial life, not tempt you to spend more than you should.

Here’s something I’ve learned that might surprise you: Sometimes the mathematically “optimal” choice isn’t the best choice for YOU. If dealing with points feels stressful or confusing, the “inferior” cash back system might actually be superior for your situation. And that’s completely okay!

Remember what I always say—personal finance is PERSONAL! The “right” choice is the one that aligns with your lifestyle, values, and financial goals.

Beyond the Rewards: The Full Financial Picture

Before we wrap up, I want to make sure we look at the whole picture. Rewards are just one part of the credit card equation, and sometimes they can distract us from more important factors.

Annual Fees vs. Benefits

Many of the most rewarding cards charge annual fees ranging from $95 to $695 or more! Before signing up, you need to do the math:

- Calculate your expected annual rewards based on your spending

- Add the value of other card benefits you’ll actually use (travel credits, lounge access, etc.)

- Subtract the annual fee

- Compare this net value to what you’d get from a no-annual-fee alternative

For example, a $95 annual fee card that earns you $300 in rewards is better than a no-annual-fee card that earns you $150. But if you’re only earning $110 with the annual fee card, you’re actually losing money!

The Interest Rate Trap

I cannot stress this enough: If there’s ANY chance you’ll carry a balance, focus on low interest rates, not rewards. According to a survey from the Federal Reserve, the average credit card interest rate is now over 24%! Even the best rewards programs only return 2-5% in value.

Do the math: If you carry a $1,000 balance for just one month at 24% APR, you’ll pay $20 in interest. That wipes out the rewards on $1,000 of spending at a 2% rate!

The Psychological Factor

Be honest with yourself about how rewards affect your spending behavior. Research from the Federal Reserve Bank of Chicago found that rewards card users spend more and carry higher balances than other cardholders.

This isn’t necessarily bad if it’s planned spending you can afford, but it’s important to recognize if rewards are subtly encouraging you to spend more than you otherwise would.

Credit Score Considerations

Opening new cards for bonuses can temporarily lower your credit score due to hard inquiries and reduced average account age. This usually isn’t significant long-term, but if you’re planning to apply for a mortgage or other important loan in the next 6-12 months, you might want to pause your rewards card applications.

Finding Your Perfect Rewards Match: Final Thoughts

We’ve covered a lot of ground today, friends! From understanding the basic differences between cash back and points to deep-diving into strategies for maximizing each system, you now have the knowledge to make an informed choice about which rewards system is best for YOUR unique situation.

Remember, there’s no one-size-fits-all answer here. For many people—especially those new to rewards cards, those who prefer simplicity, or those who don’t travel much—cash back offers the best combination of simplicity and value. The industry statistics back this up, with 58% of cardholders preferring cash back rewards.

But if you’re a frequent traveler, enjoy maximizing value through strategic redemptions, or aspire to experiences like premium cabin flights that would be cost-prohibitive with cash, a points system might offer significantly better return on your spending.

Whichever path you choose, remember these universal truths:

- No reward is worth paying interest on a credit card balance

- Your time has value too—don’t spend hours chasing minimal gains

- The best strategy is one you’ll actually follow consistently

- It’s okay to change your approach as your life circumstances change

- Financial tools should serve YOUR goals, not the other way around

Credit card rewards are a wonderful way to get something back from your everyday spending. Used wisely, they can fund vacations, offset expenses, or build savings. But they’re just one small piece of your overall financial picture. Keep them in perspective, use them intentionally, and they’ll be a blessing rather than a burden.

I’d love to hear about your experiences with different rewards systems! Which approach works best for you and why? Drop me a comment below, and let’s keep the conversation going!

Here’s to making your money work harder for YOU!

Frequently Asked Questions

1. Is it better to earn cash back or points on my credit card?

The best option depends on your personal situation. Cash back is simpler and more flexible, making it ideal if you value convenience and want to use rewards for any purpose. Points typically offer higher potential value, especially for travel, but require more knowledge to maximize. If you travel frequently and enjoy optimizing rewards, points may provide better value. If you prefer simplicity or don’t travel much, cash back is likely better.

2. Is 2% cash back the same as 2X points?

Not necessarily! 2% cash back means you earn exactly 2 cents per dollar spent. 2X points means you earn 2 points per dollar, but the value of those points depends on the rewards program and how you redeem them. In some programs, points might be worth only 0.5-0.7 cents each (making 2X points worse than 2% cash back), while in others, points could be worth 1.5-2+ cents each when strategically redeemed (making 2X points potentially worth 3-4% back).

3. How do I know if I’m getting a good value when redeeming points?

A general rule of thumb is to aim for at least 1 cent per point in value, though many programs can yield much higher values. To calculate the value, divide the cash price of what you’re getting by the number of points required. For example, if a $500 flight costs 40,000 points, that’s 1.25 cents per point ($500 ÷ 40,000 × 100). For most travel rewards programs, redeeming for flights (especially premium cabins) or transferring to hotel/airline partners typically offers the best value.

4. How many credit cards is too many?

There’s no universal answer, as it depends on your ability to manage multiple accounts responsibly. The key factors are whether you can: 1) Pay all balances in full each month, 2) Keep track of payment due dates, 3) Remember which card to use where for maximum rewards, and 4) Justify any annual fees through benefits and rewards. For most people, 2-4 carefully selected cards provide an excellent balance of rewards maximization and manageable complexity.

5. Will opening rewards credit cards hurt my credit score?

Opening new credit cards can temporarily lower your score due to hard inquiries (typically 5-10 points per inquiry) and decreased average account age. However, the increased available credit can improve your credit utilization ratio, which often has a positive effect over time. If you pay on time and keep balances low, most people can responsibly add rewards cards without significant negative impact. That said, avoid applying for new cards 6-12 months before applying for important loans like mortgages.

6. What’s the best strategy for someone just starting with rewards cards?

Start with a single, no-annual-fee cash back card that aligns with your spending patterns. After 6-12 months of responsible use, consider adding one strategic card that complements your primary spending categories. Focus on building good habits (paying in full, tracking rewards) before complexity. As you gain experience and confidence, you can explore more advanced strategies if they make sense for your situation.

7. Do rewards expire if I don’t use them?

This varies by program. Most cash back rewards don’t expire as long as your account remains open and in good standing. Points and miles policies vary widely—some expire after 12-24 months of inactivity, while others never expire. Always check your specific card’s terms and conditions. If your points do risk expiring, even a small purchase or redemption is usually enough to reset the expiration clock.

No copyright infringement is intended. All images used are copyright-free or used under Creative Commons licenses with proper attribution.