The real deal on today’s top cash back options

Last Updated: April 18, 2025

Let’s cut to the chase—cash back credit cards remain the most straightforward rewards option in an increasingly complicated financial marketplace. Unlike points or miles with their fluctuating values and byzantine redemption rules, cash back makes a simple promise: spend money, get actual money back.

But here’s the problem: with dozens of cash back cards competing for your wallet space, each with different structures, bonus categories, and fine print, finding the right card has become surprisingly complicated. I’ve spent years analyzing the cash back landscape, and I’m going to break down everything you need to know to maximize your returns without getting lost in marketing hype or leaving money on the table.

This guide cuts through the noise to help you select and optimize cash back cards that align with your real-world spending—not some imaginary ideal consumer that exists only in credit card commercials.

What Makes Cash Back Cards Different (And Why You Might Want One)

The mechanics behind your money back

Cash back credit cards are a type of rewards card that returns a percentage of your purchases to you as a straightforward rebate. While the concept sounds simple, understanding the mechanics helps you extract maximum value.

The Real Deal: How These Cards Actually Work

The process is refreshingly straightforward:

- Make a purchase: Use your cash back card for qualifying expenses

- Earn cash back: Automatically receive a percentage back as rewards

- Watch it accumulate: Cash back piles up in your account until redemption

- Cash out: Convert your cash back to statement credits, deposits, or other options

Here’s why cash back cards are different: unlike travel rewards cards with points or miles that might be worth anything from 0.5¢ to 3¢+ depending on how you redeem them, cash back offers predictable value. One percent cash back always equals one cent per dollar spent—no conversion charts or redemption tricks needed.

Why Cash Back Cards Might Be Your Best Bet

- No mental gymnastics required: Straightforward reward structure without complex point systems

- Ultimate flexibility: Cash can be used for anything, not limited to travel or specific redemptions

- Immediate gratification: No need to accumulate massive amounts before rewards become useful

- Value that doesn’t vanish overnight: Cash back value doesn’t fluctuate like points programs

- No blackout dates or availability games: Unlike travel rewards, cash back doesn’t come with restrictions

The Trade-Offs You Should Know About

- Potentially lower maximum value: May not deliver as much value as optimized points/miles for premium travel

- Annual fees on premium versions: Some enhanced cash back cards charge fees that eat into your rewards

- Category limitations: Many cards restrict higher reward rates to specific spending categories

- Redemption thresholds: Some cards make you accumulate a minimum amount (like $25) before you can cash out

- Earning caps: Cards may limit how much spending qualifies for bonus category rates

But let’s be real—the biggest advantage of cash back cards is psychological. You know exactly what you’re getting without wondering if you’re optimizing correctly or missing out on some secret high-value redemption. That clarity alone is worth something.

Breaking Down the Different Cash Back Structures

The three main approaches to cash back rewards

Cash back credit cards come in three primary flavors, each with distinct advantages and potential drawbacks. Understanding these models helps you pick the option that aligns with your spending habits and reward preferences.

1. Flat-Rate Cards: The “Set It and Forget It” Option

How flat-rate rewards work in practice

How flat-rate rewards work in practice

Flat-rate cards offer the same reward percentage on everything you buy, regardless of what it is or where you get it.

The Essentials:

- Consistent earnings: Typically 1.5-2% cash back on absolutely everything

- No category juggling: Same rate applies whether you’re buying groceries or garage door openers

- No activation hoops: Rewards accumulate automatically without quarterly sign-ups

- No earning limits: Usually no caps on how much cash back you can rack up

Who Should Get One: Flat-rate cards are perfect for people with varied spending that doesn’t concentrate heavily in common bonus categories. They’re also ideal if you prefer simplicity over slightly higher rewards that require more management. If you want a “set it and forget it” approach, these cards are your best friend.

Popular Examples:

- Citi Double Cash® Card (2% total: 1% when you buy, 1% when you pay)

- Wells Fargo Active Cash® Card (2% cash rewards on everything)

- Capital One Quicksilver Cash Rewards (1.5% cash back, no fuss)

2. Tiered Category Cards: The Specialist Approach

How tiered rewards target specific spending

Tiered cash back cards offer higher reward rates in specific spending categories and a lower base rate on everything else.

The Essentials:

- Juiced-up rewards: Higher percentages (often 3-6%) in selected categories

- Consistent categories: Bonus categories remain the same year-round

- Base earnings: Lower rate (typically 1%) on purchases outside your bonus categories

- Category limits: Many cards cap bonus earnings in specific categories

Who Should Get One: These cards shine for people with predictable spending in common bonus categories like groceries or gas. They’re great if you’re willing to use multiple cards strategically for different purchases but don’t want to deal with quarterly changes. If your spending heavily concentrates in a few specific categories, these cards often provide the highest total return.

Popular Examples:

- Blue Cash Preferred® from American Express (6% at U.S. supermarkets up to $6,000/year, 6% on select streaming services, 3% on transit and U.S. gas stations, 1% elsewhere)

- Chase Freedom Unlimited® (5% on travel purchased through Chase, 3% on dining and drugstores, 1.5% on everything else)

- Bank of America® Customized Cash Rewards (3% in your choice category, 2% at grocery stores and wholesale clubs, 1% on other purchases)

3. Rotating Category Cards: The Maximizer’s Game

How rotating categories work throughout the year

Rotating category cards offer high cash back rates in categories that change periodically (typically quarterly), with a lower base rate on everything else.

The Essentials:

- Eye-popping bonus rates: Typically 5% cash back in featured categories

- Quarterly shuffle: Categories change every three months

- Manual activation required: You must opt in each quarter to get bonus rewards

- Spending caps: Usually limited to $1,500 in combined quarterly category spending

- Baseline earnings: 1% on everything that doesn’t fit the quarterly theme

Who Should Get One: These cards reward people willing to track changing categories and adjust their spending accordingly. They’re ideal if you can time large purchases to align with relevant categories and don’t mind a bit more active management. If you enjoy playing the rewards game and maximizing returns, these cards can deliver substantial value.

Popular Examples:

- Chase Freedom Flex℠ (5% on rotating quarterly categories up to $1,500)

- Discover it® Cash Back (5% on quarterly categories up to $1,500)

- Citi Custom Cash℠ Card (5% on your top spending category each billing cycle up to $500)

4. Hybrid Cash Back Cards: The Best of Both Worlds

Some cards blend elements of multiple structures to create flexible cash back models that defy simple categorization.

The Essentials:

- Blended approach: Combines features from different cash back structures

- Customization options: Some allow you to personalize bonus categories

- More moving parts: May require more active management than simpler card types

Who Should Get One: Hybrid cards appeal to people seeking flexibility and higher potential rewards who don’t mind learning and optimizing more complex reward structures. They’re perfect if your spending patterns don’t fit neatly into traditional models or if you want more control over your reward categories.

Popular Examples:

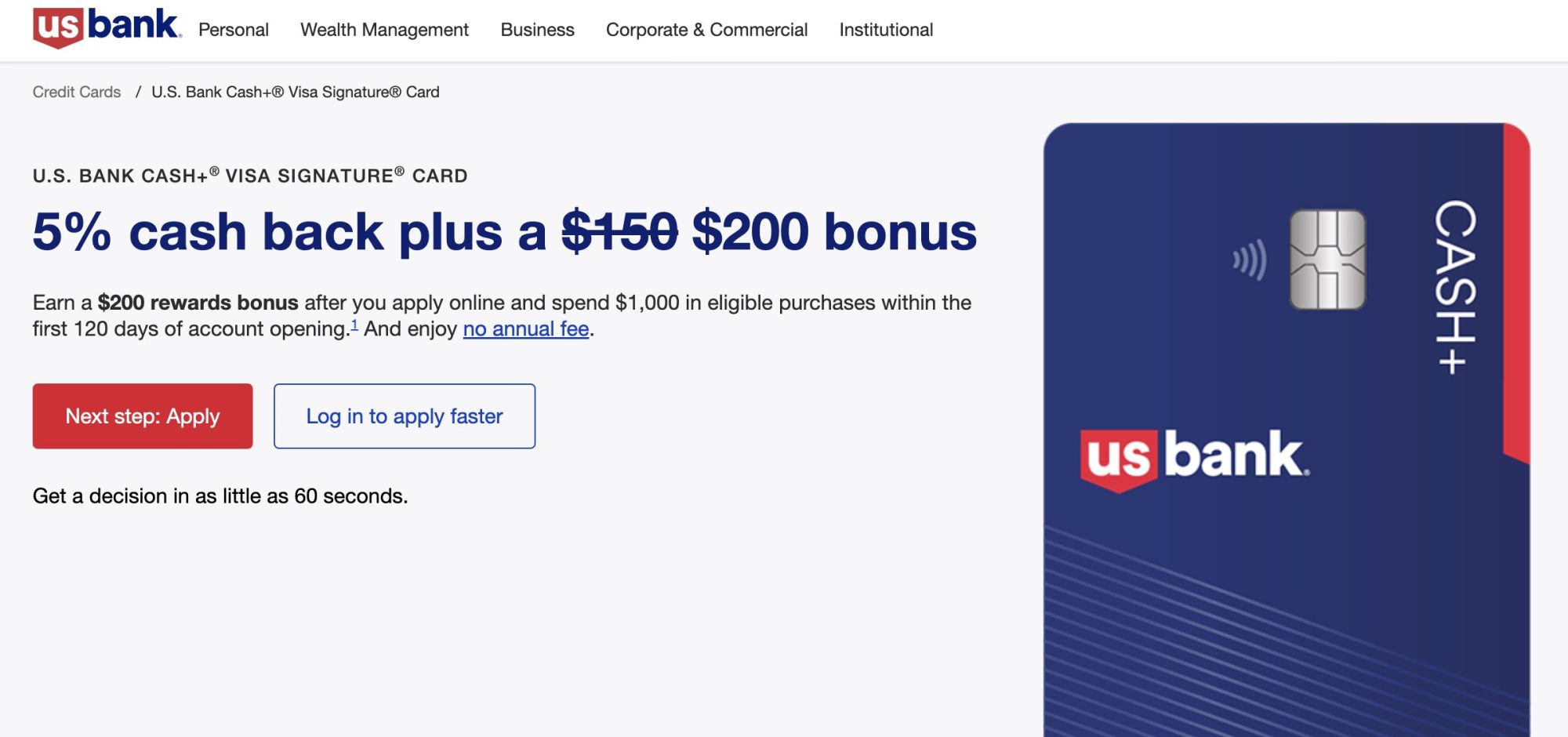

- U.S. Bank Cash+® Visa Signature® Card (5% on two categories you choose up to $2,000 quarterly, 2% on one everyday category, 1% elsewhere)

- Bank of America® Customized Cash Rewards (3% in your choice category, 2% at grocery stores and wholesale clubs, 1% on everything else)

- Citi Custom Cash℠ Card (5% on your top eligible spend category each billing cycle up to $500, 1% on everything else)

Wait—here’s the kicker: the “best” structure isn’t universal. It depends entirely on your specific spending patterns and how much effort you’re willing to invest in managing your rewards. A rotating category card might offer the highest theoretical return, but if you forget to activate the categories each quarter, a simple flat-rate card will actually put more money in your pocket.

The Cash Back Credit Cards Actually Worth Your Time in 2025

Today’s standout performers across categories

Today’s standout performers across categories

I’ve analyzed dozens of cash back cards, weighing earning potential, fees, welcome bonuses, and extra perks. Here are the cards that truly deliver value across different categories as of April 2025.

Top Flat-Rate Cash Back Cards

Citi Double Cash® Card: The Gold Standard

- Cash Back Rate: 2% total on everything (1% when you buy, 1% when you pay)

- Annual Fee: $0

- Welcome Bonus: $200 cash back after spending $1,500 in first 3 months

- Why It’s Great:

- No categories to track or activate—just consistent rewards

- Strong 0% intro APR on balance transfers (18 months)

- No annual fee to justify

- Who Should Get It: Anyone wanting maximum simplicity without sacrificing reward rate

Wells Fargo Active Cash® Card: The Straightforward Earner

- Cash Back Rate: Unlimited 2% cash rewards on purchases

- Annual Fee: $0

- Welcome Bonus: $200 cash rewards after spending $1,000 in first 3 months

- Why It’s Great:

- Straightforward 2% back with no hoops to jump through

- Cell phone protection (up to $600) just for paying your bill with the card

- Solid intro APR offers on both purchases and balance transfers

- Who Should Get It: People who want strong flat-rate rewards plus phone protection

Capital One Quicksilver Cash Rewards Credit Card: The No-Fuss Option

- Cash Back Rate: Unlimited 1.5% cash back on every purchase

- Annual Fee: $0

- Welcome Bonus: $200 cash bonus after spending $500 in first 3 months

- Why It’s Great:

- Low spending requirement for the welcome bonus

- No foreign transaction fees (rare for a cash back card)

- Extended warranty coverage on eligible purchases

- Who Should Get It: Occasional international travelers who want simplicity

Best Tiered Category Cash Back Cards

Blue Cash Preferred® Card from American Express: The Grocery Champion

- Cash Back Rate:

- 6% at U.S. supermarkets (up to $6,000 per year)

- 6% on select U.S. streaming services

- 3% on transit and U.S. gas stations

- 1% on everything else

- Annual Fee: $95

- Welcome Bonus: $350 statement credit after spending $3,000 in first 6 months

- Why It’s Great:

- Industry-leading grocery rewards rate

- Excellent for families with high grocery and streaming expenses

- Return protection that most people don’t know about

- Who Should Get It: Households spending at least $3,200 annually on groceries

Chase Freedom Unlimited®: The Versatile Workhorse

- Cash Back Rate:

- 5% on travel booked through Chase Travel℠

- 3% on dining and drugstore purchases

- 1.5% on everything else

- Annual Fee: $0

- Welcome Bonus: $200 bonus after spending $500 in first 3 months

- Why It’s Great:

- Solid earnings on common spending categories

- No annual fee despite the enhanced category rates

- Part of the valuable Chase Ultimate Rewards ecosystem

- Who Should Get It: People wanting enhanced rewards in everyday categories without paying a fee

U.S. Bank Altitude® Connect Visa Signature® Card: The Travel & Gas Powerhouse

- Cash Back Rate:

- 5x points on hotels and car rentals booked through Altitude Rewards Center

- 4x points on travel and gas stations

- 2x points on groceries, dining, and streaming

- 1x point on everything else

- Annual Fee: $95 (waived first year)

- Welcome Bonus: 50,000 bonus points after spending $3,000 in first 120 days

- Why It’s Great:

- Annual $30 streaming service credit

- Cell phone protection up to $600

- No foreign transaction fees

- Who Should Get It: Commuters and travelers who can maximize the 4x categories

Top Rotating Category Cash Back Cards

Chase Freedom Flex℠: The Category Chameleon

- Cash Back Rate:

- 5% on rotating quarterly categories (up to $1,500 in combined purchases)

- 5% on travel purchased through Chase Travel℠

- 3% on dining and drugstore purchases

- 1% on everything else

- Annual Fee: $0

- Welcome Bonus: $200 bonus after spending $500 in first 3 months

- Why It’s Great:

- Combines rotating and fixed bonus categories

- Cell phone protection (rare for a no-annual-fee card)

- Trip cancellation/interruption insurance

- Who Should Get It: Rewards optimizers who want to maximize categories while having solid fixed bonuses

Discover it® Cash Back: The First-Year Doubler

- Cash Back Rate:

- 5% on rotating quarterly categories (up to $1,500 in combined purchases)

- 1% on everything else

- Cashback Match® (all cash back earned in first year is doubled)

- Annual Fee: $0

- Welcome Bonus: Cashback Match® (effectively doubles your first-year earnings)

- Why It’s Great:

- First-year match makes effective earn rate 10% in categories, 2% elsewhere

- No foreign transaction fees

- Free FICO® Score monitoring

- Who Should Get It: New cardholders who can maximize first-year earnings

Citi Custom Cash℠ Card: The Autopilot Maximizer

- Cash Back Rate:

- 5% on your top eligible spend category each billing cycle (up to $500)

- 1% on everything else

- Annual Fee: $0

- Welcome Bonus: $200 cash back after spending $1,500 in first 6 months

- Why It’s Great:

- Automatically adjusts to your spending pattern each month

- No activation required—the 5% applies to your highest category

- 0% intro APR for 15 months on purchases and balance transfers

- Who Should Get It: People who want category maximization without tracking or activating

Special-Purpose Cash Back Cards

American Express Blue Cash Everyday® Card: The No-Fee Grocery Option

- Cash Back Rate:

- 3% at U.S. supermarkets (up to $6,000 per year)

- 3% on U.S. online retail purchases (up to $6,000 per year)

- 3% at U.S. gas stations (up to $6,000 per year)

- 1% on other purchases

- Annual Fee: $0

- Welcome Bonus: $250 statement credit after spending $2,000 in first 6 months

- Why It’s Great:

- Strong grocery rate without an annual fee

- $180 Home Chef credit ($15 monthly)

- $84 Disney Bundle credit ($7 monthly)

- Who Should Get It: Moderate grocery shoppers who can’t justify the Preferred version’s annual fee

Bank of America® Customized Cash Rewards Card: The Flexible Specialist

- Cash Back Rate:

- 3% in choice category (gas, online shopping, dining, travel, drugstores, or home improvement)

- 2% at grocery stores and wholesale clubs

- 1% on everything else

- (3% and 2% categories limited to $2,500 in combined quarterly purchases)

- Annual Fee: $0

- Welcome Bonus: $200 online cash rewards after spending $1,000 in first 90 days

- Why It’s Great:

- Change your 3% category once per month as needs shift

- No annual fee despite the flexibility

- Preferred Rewards members earn 25-75% more cash back

- Who Should Get It: People whose spending priorities change regularly

Capital One SavorOne Cash Rewards Credit Card: The Entertainment Enthusiast’s Pick

- Cash Back Rate:

- 3% on dining, entertainment, popular streaming services, and grocery stores

- 5% on hotels and rental cars booked through Capital One Travel

- 1% on everything else

- Annual Fee: $0

- Welcome Bonus: $200 cash bonus after spending $500 in first 3 months

- Why It’s Great:

- Rare to find entertainment as a bonus category

- No foreign transaction fees

- Solid intro APR offer

- Who Should Get It: Diners and entertainment seekers (concerts, movies, sporting events)

How to Choose the Right Cash Back Card (Without Going Crazy)

Selecting the ideal cash back card isn’t about finding the “best” card—it’s about finding the best card for your specific situation. Here’s a practical approach to cutting through the marketing hype and identifying a card that genuinely matches your needs.

Step 1: Get Real About Your Spending Habits

The foundational step is understanding where your money actually goes:

- Track your spending: Review 3-6 months of expenses to identify your top spending categories

- Run the numbers: Calculate monthly and yearly totals for each category

- Look for patterns: Determine if your spending is heavily concentrated in a few categories or spread broadly

- Consider seasonality: Does your spending pattern change significantly throughout the year?

This analysis is gold because it shows you which bonus categories will actually put money back in your pocket, not just sound good in theory.

For example, that impressive 6% back on U.S. supermarkets might look amazing, but if you’re spending just $100 monthly on groceries while dropping $500 at restaurants, a dining rewards card would be more valuable for you.

Step 2: Match Card Structures to Your Spending

Based on your spending analysis, identify which cash back structure aligns best:

- If your spending is widely distributed across many categories: → Consider a flat-rate card offering 1.5-2% on everything

- If your spending heavily concentrates in common bonus categories (groceries, gas, dining): → Consider a tiered category card with enhanced rewards in those specific areas

- If you can be flexible about when you make certain purchases: → Consider a rotating category card with 5% in changing quarterly categories

- If you have significant spending in multiple specific categories: → Consider a card that allows category choice or multiple cards for different purposes

Let’s run an example calculation for someone spending $2,000 monthly:

- Flat-rate card (2%): $480 annual cash back

- Tiered card (4% in categories representing half your spending, 1% elsewhere): $600 annual cash back

The right structure depends entirely on your unique spending pattern—there’s no one-size-fits-all solution.

Step 3: Annual Fee Math: Worth It or Not?

Many premium cash back cards charge annual fees. Here’s how to determine if they’re justified:

- Calculate the break-even point: Annual Fee ÷ (Premium Card Rate – No-Fee Card Rate) = Break-even Spending

- Example: Blue Cash Preferred® ($95 fee, 6% groceries) vs. Blue Cash Everyday® (no fee, 3% groceries) $95 ÷ (6% – 3%) = $3,167 annual grocery spending to break even

- Factor in other benefits:

- Statement credits that offset the fee

- Insurance benefits you would otherwise pay for

- Enhanced redemption options

- Welcome bonuses that might justify the fee for the first year

- Be ruthlessly honest: Only count benefits you’ll actually use, not theoretical value

A card with an annual fee only makes sense if your real-world usage generates more rewards than a no-fee alternative, after accounting for the fee.

Step 4: Redemption Options and Minimums

Different cards offer various ways to access your cash back:

- Statement credits: Applied directly to your card balance

- Direct deposits: Transferred to your linked checking or savings account

- Physical checks: Mailed to your address upon request

- Gift cards: Sometimes available at enhanced values

- Charitable donations: Convert rewards to charitable contributions

Also consider these practical factors:

- Redemption minimums: Some cards require you to accumulate $25-50 before redeeming

- Automatic redemption: Some cards offer convenient monthly automatic redemption

- Expiration policies: Verify whether rewards expire if unused

Your preference for how and when you can access your rewards should factor into your decision, especially if you prefer frequent small redemptions.

Step 5: Your Credit Profile Reality Check

Your credit score and history will determine which cards you can actually qualify for:

- Excellent credit (740+): Access to all premium cash back cards

- Good credit (670-739): Eligible for many competitive cash back cards

- Fair credit (580-669): Limited options, but some cash back cards are available

- Poor credit (below 580): May need to start with a secured card before qualifying for cash back cards

There’s no sense fantasizing about a card you can’t qualify for. Check your credit score before applying and target cards aligned with your credit profile to avoid unnecessary rejections.

Step 6: Welcome Bonus Considerations

Welcome bonuses provide substantial upfront value but should be viewed as a bonus rather than the primary decision factor:

- Bonus amount: Cash back bonuses typically range from $150-350

- Spending requirement: Ensure you can meet the minimum spend naturally

- Time frame: Check how long you have to meet the requirement

- Eligibility rules: Review restrictions (like previous cardholder exclusions)

Example analysis:

- $200 bonus requiring $1,000 spend in 3 months = 20% return on that initial spending

- This significantly enhances first-year value but doesn’t affect ongoing rewards

Step 7: Additional Benefits Worth Considering

Look beyond the cash back structure to assess complementary benefits:

- 0% intro APR offers: Valuable if you need to finance a large purchase or transfer a balance

- Purchase protection: Coverage if items you buy are damaged or stolen

- Extended warranty: Additional coverage beyond manufacturer’s warranty

- Cell phone protection: Insurance for your phone when you pay your bill with the card

- Foreign transaction fees: Important if you travel internationally

- Travel benefits: Rental car insurance, trip cancellation coverage, etc.

These “side benefits” can enhance a card’s overall value, especially if they replace services you’d otherwise pay for separately.

Step 8: Your Complexity Tolerance

Be honest about how much effort you’re willing to put into maximizing rewards:

- Low maintenance preference: Choose a flat-rate card with simple redemption

- Moderate effort tolerance: Consider tiered category cards with fixed bonus categories

- High optimization interest: Explore rotating category cards or multi-card strategies

The theoretically most rewarding strategy often involves multiple cards, but this requires more active management. Choose a level of complexity that realistically matches your interest and organizational skills.

Maximizing Your Cash Back Without Making It a Second Job

Practical strategies to boost your earnings

Once you’ve chosen the right cash back card(s), implementing these straightforward approaches can help you squeeze more value from your rewards without turning card management into a part-time job.

The Right Card for Each Purchase: Strategic Usage

Develop a system for using the optimal card for each spending category:

- Create a quick reference guide: A wallet-sized cheat sheet or phone note listing which card to use where

- Use visual cues: Small stickers or markings to identify each card’s primary purpose

- Set up digital wallets properly: Designate default cards for different merchant types

- Organize recurring payments: Assign subscription services and bill payments to appropriate category cards

Here’s what an optimized strategy might look like:

- Groceries → Blue Cash Preferred® (6%)

- Dining → Chase Freedom Unlimited® (3%)

- Gas → U.S. Bank Altitude Connect (4x)

- Everything else → Citi Double Cash® (2%)

This approach sounds complicated but quickly becomes second nature. The key is creating simple systems that don’t require constant decision-making.

Rotating Category Maximization: Calendar-Based Strategy

For cards with rotating quarterly bonus categories:

- Set calendar alerts: Create notifications for category activation periods

- Plan major purchases: Time discretionary spending to align with relevant categories

- Stock up strategically: Purchase gift cards or non-perishable items during bonus periods

- Prepay when possible: Pay bills in advance when they fall in bonus categories

For example, if Chase Freedom Flex℠ features 5% at grocery stores in Q1:

- Stock up on household essentials that won’t expire

- Purchase gift cards for restaurants and retailers you regularly visit

- Prepay streaming services if possible

Multi-Card Strategy: The Power of Complementary Cards

For those comfortable managing multiple cards:

- Choose non-overlapping cards: Select cards with different bonus categories

- Designate a base card: Identify your highest flat-rate card for non-bonus spending

- Manage annual fees carefully: Ensure premium cards deliver value exceeding their fees

- Space out applications: Apply for new cards strategically to maximize welcome bonuses

An effective three-card strategy might include:

- American Express Blue Cash Preferred® for groceries and streaming

- Chase Freedom Flex℠ for rotating categories and dining

- Citi Double Cash® for everything else

This approach lets you earn 3-6% in major categories while still getting 2% on everything else—a significant improvement over using a single card.

Bonus Earning Hacks: Beyond the Basics

Enhance your standard cash back with these additional techniques:

- Issuer shopping portals: Earn additional cash back by shopping through your card’s online portal

- Card-linked offers: Activate and use Amex Offers, Chase Offers, BankAmeriDeals, etc.

- Dining programs: Register your cards in programs that provide extra rewards at restaurants

- Stacking opportunities: Combine card rewards with store loyalty programs and rebate apps

Example reward stack:

- Base card reward: 2% cash back = $2 on $100 purchase

- Shopping portal bonus: 5% extra = $5

- Card-linked offer: $10 off $50 = $10

- Total rewards: $17 on $100 purchase (17% effective return)

These stacking opportunities often fly under the radar but can substantially boost your overall returns.

Welcome Bonus Maximization: Timing Is Everything

Welcome bonuses often represent the largest single reward opportunity:

- Track progress toward spending requirements: Monitor your progress to ensure you hit thresholds

- Time applications around planned large purchases: Apply before major expenses

- Add authorized users when rewarded: Some cards offer bonuses for adding users

- Explore referral opportunities: Earn additional cash back by referring friends and family

A strategic approach to welcome bonuses can add hundreds of dollars to your annual rewards—just don’t chase bonuses at the expense of your credit health.

Category Cap Management: Watch Your Limits

Many cards limit bonus earnings in specific categories:

- Track category spending: Monitor progress toward caps using your card’s app or website

- Switch cards strategically: Change to another card once you hit category limits

- Time annual purchases: Schedule major category purchases early in your membership year

- Know your reset dates: Understand when your quarterly or annual limits refresh

For example, with Blue Cash Preferred® (6% groceries up to $6,000 annually):

- Track grocery spending as it approaches the $6,000 limit

- Switch to another grocery bonus card after reaching the limit

- Plan annual grocery spending to maximize the 6% category

Advanced Redemption Techniques

Some cash back programs offer enhanced value for certain redemption options:

- Redemption bonuses: Watch for special promotions offering bonuses for redeeming

- Gift card promotions: Some programs offer gift cards at discounted point rates

- Minimum threshold efficiency: Accumulate enough rewards to clear redemption minimums

- Timing opportunities: Some programs offer enhanced redemption value during promotions

For example:

- Wait until you have $25 in rewards if your program has a minimum redemption threshold

- Look for gift card promotions that offer better than 1:1 value

Pairing with Store Loyalty Programs: Double-Dipping

Enhance cash back by combining with merchant-specific programs:

- Retail loyalty programs: Join free rewards programs at places you shop frequently

- Receipt scanning apps: Use apps like Fetch Rewards or Ibotta for additional rebates

- Wholesale club rewards: Combine cash back with membership rewards at Costco, Sam’s Club, etc.

- Fuel rewards programs: Stack gas station loyalty with credit card rewards

This layered approach can generate remarkable returns. A grocery trip might earn:

- Credit card reward: 6% cash back

- Store loyalty: 2% in store points

- Receipt scanning: 1-3% in specific item rebates

- Total potential return: 9-11% on grocery spending

Annual Fee Optimization: Getting Your Money’s Worth

For cards with annual fees, maximize value through strategic timing:

- Use all statement credits: Set reminders to ensure you utilize all available credits

- Request retention offers: Contact the issuer before renewal to inquire about retention bonuses

- Consider downgrade options: Product changes to no-annual-fee versions can preserve history

- Look for upgrade opportunities: Watch for targeted offers with enhanced bonuses

For example, with American Express Blue Cash Preferred® ($95 fee):

- Ensure you maximize the 6% grocery category up to $6,000 yearly

- Fully utilize the 6% streaming benefit

- Evaluate whether your actual rewards exceed the fee plus what you’d earn with a no-fee alternative

Cash Back vs. Points/Miles: Which Actually Delivers More Value?

:max_bytes(150000):strip_icc()/4230530_final-691192e3e2a04cf5be496ce51d664ff2.png) The real comparison between cash and travel rewards

The real comparison between cash and travel rewards

When choosing a rewards credit card, you’ll inevitably face the fundamental question: cash back or points/miles? Both have distinct advantages and potential drawbacks, making this a highly personal decision based on your lifestyle, preferences, and financial goals.

The Core Differences: What Sets Them Apart

Value Transparency

Cash Back:

- Fixed value: Consistently worth 1 cent per percentage point

- Predictable returns: Easy to calculate exact reward value

- Stable worth: Value doesn’t fluctuate over time

- Universal utility: Cash works for literally anything

Points/Miles:

- Variable value: Typically 0.5-3+ cents per point depending on redemption

- Redemption-dependent: Value varies based on how you use points

- Potential upside: Strategic redemptions can yield 2-5+ cents per point

- Devaluation risk: Programs can change redemption rates with little notice

Complexity Comparison

Cash Back:

- Dead simple: Straightforward percentage-based rewards

- Effortless redemption: Often automatic or requires minimal steps

- No learning curve: Minimal research needed

- Low maintenance: Set-and-forget approach works fine

Points/Miles:

- More moving parts: Understanding transfer partners, award charts, etc.

- Research intensive: Finding high-value redemptions takes work

- Steeper learning curve: Requires knowledge of loyalty programs

- Active management: Regular monitoring for optimal opportunities

Travel Utility

Cash Back:

- Ultimate flexibility: Use rewards for travel or anything else

- No blackout dates: Book travel whenever and however you want

- Easy comparison shopping: Simple to compare cash prices

- Compatible with deals: Can be used alongside travel promotions

Points/Miles:

- Travel-focused perks: Often includes benefits beyond just points

- Premium access: Can enable luxury travel otherwise unaffordable

- Transfer opportunities: Potential for outsized value via partners

- Special availability: Sometimes access to award space unavailable for cash

When Cash Back Is Clearly Better

Cash back cards generally win in these scenarios:

1. You Value Simplicity Above All

If you hate complicated systems and just want straightforward rewards without having to learn program details or monitor redemption opportunities, cash back eliminates all that mental overhead.

2. You Travel Occasionally or Unpredictably

Infrequent travelers often can’t accumulate enough points for meaningful redemptions, or may not travel enough to justify cards with travel-focused annual fees. Cash back provides immediate value regardless of travel frequency.

3. You’re a Budget Travel Enthusiast

If you typically hunt for the cheapest flights, stay in budget accommodations, or prefer road trips, cash back allows you to book the lowest-cost options while still earning rewards, rather than being tied to specific loyalty programs.

4. You Want Ultimate Flexibility

Cash rewards provide unmatched versatility—they can fund travel when desired but can also cover everyday expenses, emergencies, or even be invested. This flexibility is particularly valuable during changing financial circumstances.

5. You Prefer Predictability Over Potential

Unlike points programs that can be devalued overnight, cash back maintains consistent value. If you prefer guaranteed, predictable returns on your spending without worrying about program changes, cash back eliminates the uncertainty.

When Points and Miles Pull Ahead

Points and miles programs typically deliver better value in these situations:

1. You’re a Frequent Traveler

Regular travelers can accumulate significant points balances and take advantage of the travel-specific perks bundled with travel rewards cards, such as lounge access, free checked bags, or elite status benefits.

2. You Aspire to Premium Travel Experiences

If you dream of business class flights or luxury hotel stays that would otherwise be financially out of reach, points can provide access to these experiences at a fraction of the cash cost—often delivering 3-5+ cents per point in value.

3. You Enjoy Optimization as a Hobby

For those who actually enjoy learning program details and finding maximization opportunities, points and miles can be significantly more rewarding than cash back for the same spending. Some people genuinely find this process fun rather than tedious.

4. You Have Flexible Travel Plans

If you can adjust travel dates or destinations based on award availability, you’ll extract maximum value from points programs by booking during optimal redemption windows or taking advantage of limited-time transfer bonuses.

5. You Travel Internationally

Many travel rewards cards include valuable international benefits like no foreign transaction fees, global lounge access, and comprehensive travel insurance that can save substantial money on international trips.

A Real-World Value Comparison

To illustrate the potential difference in value, let’s compare a premium cash back card with a travel rewards card:

Scenario: $30,000 Annual Spending

Cash Back Option: Blue Cash Preferred®

- 6% on $6,000 groceries = $360

- 3% on $3,000 gas = $90

- 1% on $21,000 other spending = $210

- Less $95 annual fee

- Net rewards: $565 (1.88% effective return)

Travel Rewards Option: American Express Gold Card

- 4x on $6,000 groceries = 24,000 points

- 4x on $5,000 dining = 20,000 points

- 1x on $19,000 other spending = 19,000 points

- Total: 63,000 points

- Valued at 1.0¢ each for statement credits = $630

- Valued at 2.0¢ each for strategic travel transfers = $1,260

- Less $250 annual fee

- Plus $240 in dining/Uber credits (if fully utilized)

- Net rewards: $380 for cash redemption (1.27% effective return)

- Net rewards: $1,010 for optimized travel redemption (3.37% effective return)

This example illustrates how travel points can potentially deliver significantly higher value when used optimally for travel, but may underperform cash back when redeemed for non-travel options or if credits go unused.

The Smart Hybrid Approach

Many savvy consumers adopt a balanced approach using both card types:

- Cash back for everyday spending: Use cash back cards for regular expenses and non-bonus categories

- Points cards for travel spending: Use travel rewards cards for travel-related purchases and categories that earn bonus points

- Strategic welcome bonuses: Apply for cards with valuable sign-up offers that align with upcoming needs

- Complementary benefits: Choose cards whose benefits address different aspects of your financial life

This balanced strategy provides the simplicity and flexibility of cash back for everyday needs while preserving the opportunity for high-value travel redemptions when desired.

Questions People Actually Ask About Cash Back Cards

Real answers to common cash back confusion

Real answers to common cash back confusion

Redemption Questions

“How exactly do I get my cash back? Does it automatically apply to my bill?”

The redemption process varies by issuer, but most offer several options:

- Statement credits: Applied to reduce your card balance (most common)

- Direct deposits: Transferred to your linked checking or savings account

- Paper checks: Physically mailed to your address

- Gift cards: Converted to merchant gift cards (sometimes at enhanced value)

- Merchandise: Redeemed through issuer shopping portals (typically poor value)

Some cards offer automatic redemption at certain thresholds, while others require manual redemption through your online account or mobile app. Check your specific card’s terms for available options.

“Is there a minimum amount I need to accumulate before redeeming?”

Many cash back programs have minimum redemption thresholds:

- No minimum: Some cards like Capital One Quicksilver allow redemption of any amount

- Low threshold: Common minimums range from $20-25 (Chase, American Express)

- Higher minimums: Some programs require $50+ for certain redemption options

These thresholds often vary based on your chosen redemption method—statement credits typically have lower minimums than physical checks. Always check your specific card’s policies, as they change periodically.

“Do cash back rewards expire if I don’t use them?”

Expiration policies vary significantly between issuers:

- No expiration: Many major issuers (Chase, Capital One, Discover) have eliminated cash back expiration as long as your account remains open and in good standing

- Inactivity expiration: Some programs expire rewards after extended periods without card use (typically 12-24 months)

- Time-based expiration: Less common today, but some programs still expire rewards after a set period regardless of activity

- Account closure: Nearly all programs forfeit unredeemed rewards when you close your account

To protect your hard-earned cash back, maintain regular account activity and set reminders if your program has expiration policies. When closing a card, always redeem available cash back first.

“Can I convert my cash back to travel points or other rewards?”

Transfer options vary by issuer and card family:

- Within same issuer/program: Often allowed between cards in the same rewards ecosystem (e.g., Chase Ultimate Rewards cards)

- Between different issuers: Generally impossible to transfer directly between competitors

- To other people: Some programs allow transfers to household members

- Between reward types: Some flexible programs allow conversion between cash back and points

For example, the Chase Freedom Flex℠ earns “cash back” that’s technically Ultimate Rewards points, which can be transferred to a Sapphire Preferred® for enhanced travel value. American Express, however, keeps their Membership Rewards and cash back programs separate.

Earning and Maximizing Questions

“Why did I get less cash back than expected on a purchase?”

There are several common reasons for unexpected reward amounts:

- Merchant category misclassification: The store’s payment system might be categorized differently than expected

- Partial category exclusions: Some stores may be partially excluded from bonus categories

- Promotional period timing: Purchase might have fallen outside a promotional period

- Spending cap reached: You may have exceeded a category spending limit

- Reward calculation timing: Some issuers calculate rewards at statement close rather than transaction time

Most modern card apps show pending rewards per transaction, making it easier to spot when something doesn’t match expectations. If you suspect an error, contact your issuer—they can sometimes manually adjust miscategorized purchases.

“Do returns affect my cash back earnings?”

Yes, when you return an item, the issuer claws back the associated cash back:

- Reward reversal: Cash back earned on the original purchase gets deducted

- Statement adjustment: Usually appears as a negative entry in your rewards summary

- Timing differences: May occur in a different billing cycle than the original purchase

- Redemption complications: If you’ve already redeemed the rewards, the issuer may deduct from future earnings

This system ensures rewards are only earned on final purchases. The reversal process is typically automatic and applies even for partial returns.

“Do all purchases earn cash back rewards?”

Not all transactions qualify for cash back rewards. Common exclusions include:

- Cash-like transactions: Cash advances, money orders, cryptocurrency, gambling

- Balance transfers: Moving debt between cards

- Person-to-person payments: Some P2P transfers may not qualify

- Financial institution payments: Mortgage or loan payments through certain channels

- Annual fees and interest: Card fees and interest charges never earn rewards

Additionally, purchases must be correctly categorized by the merchant’s payment system to earn category bonuses. Always check your card’s terms and conditions for specific exclusion details.

“How are purchases categorized for bonus cash back?”

Purchase categorization depends on the merchant category code (MCC) assigned to each business:

- Payment networks assign codes: Visa, Mastercard, Amex, and Discover classify businesses

- Business type determines category: Based on the merchant’s primary business, not specific items purchased

- Surprising classifications: Some businesses may fall under unexpected categories

For example, a gas station convenience store might be coded as either “gas” or “grocery” depending on its primary business. Card issuers generally can’t override these classifications for individual transactions.

Financial and Credit Questions

“Will applying for a cash back card hurt my credit score?”

Applying for any credit card, including cash back cards, affects your credit score in several ways:

- Hard inquiry impact: Typically causes a small, temporary drop (about 5-10 points)

- New account effect: Reduces your average account age if approved

- Available credit increase: Additional credit can improve your utilization ratio

- Payment history opportunity: Future on-time payments strengthen your score

For most people with established credit, the initial negative impact is small and temporary, while the long-term effect is often positive if the card is managed responsibly. Multiple applications in a short period, however, can cause more significant damage.

“Do cash back cards have higher interest rates than regular cards?”

Yes, cash back and other rewards cards typically carry higher APRs than basic cards:

- Rate premium: Usually 2-5 percentage points higher than no-frills cards

- Rewards funding: Higher rates help subsidize those rewards

- Target audience: Rewards cards aim at consumers who spend more and pay in full

- Alternative options: If you carry balances, low-interest cards are almost always better financially

This highlights why paying your balance in full each month is absolutely crucial with cash back cards. Interest charges quickly devour any rewards earned—even at high cash back rates.

“Can I have multiple cash back cards from the same issuer?”

Yes, most issuers allow customers to hold multiple cash back cards simultaneously:

- Portfolio diversification: Different cards can cover various bonus categories

- Welcome bonus opportunities: May qualify for multiple sign-up bonuses (with restrictions)

- Issuer limits: Some banks cap the total number of their cards you can hold

- Application timing: Too many applications with one issuer in a short period may trigger rejections

A strategic approach might involve holding complementary cards from the same issuer—like the Blue Cash Preferred® and Blue Cash Everyday® from American Express to maximize grocery spending across their combined caps.

“Is it worth paying an annual fee for a cash back card?”

It depends entirely on your spending patterns and the card’s benefits:

- Break-even analysis: Calculate minimum spending needed to offset the fee compared to no-fee alternatives

- Benefit valuation: Consider the value of additional perks beyond cash back

- Welcome bonus impact: First-year bonuses often easily justify the initial fee

- Usage alignment: Assess whether your spending matches the card’s bonus categories

For example, the Blue Cash Preferred® ($95 annual fee) makes financial sense for someone spending over $3,200 annually at U.S. supermarkets compared to its no-fee counterpart. For someone who rarely cooks at home, it would be a poor choice despite the impressive 6% grocery rate.

Strategy Questions

“Should I get multiple cash back cards or stick with one good card?”

The answer depends on your spending patterns and tolerance for complexity:

Multiple card advantages:

- Higher effective rewards across various categories

- Ability to maximize different bonus categories

- Often lower overall annual fees

- Backup options if one card isn’t accepted

Single card advantages:

- Simplicity of management

- Consolidated rewards in one program

- Less mental overhead when making purchases

- Easier to track expenses

For many people, a strategic combination of 2-3 complementary cards hits the sweet spot—maximizing rewards without creating a management nightmare. If you value simplicity above all, a strong flat-rate card (1.5-2%) is probably your best bet.

“How do I maximize value with rotating category cards?”

To optimize cards like Chase Freedom Flex℠ or Discover it® Cash Back:

- Set calendar alerts to remind you when to activate new quarterly categories

- Plan major purchases around relevant bonus categories

- Buy gift cards for places you’ll shop later when they fall in bonus categories

- Track spending to ensure you reach but don’t exceed category limits

- Pair with other cards to maximize non-category purchases

This approach requires more active management but can yield significantly higher rewards for those willing to stay organized. For extra credit, review historical category patterns to predict and plan for future quarters.

“Should I choose cash back or a 0% APR offer?”

It depends on your immediate financial needs:

- If carrying a balance: When financing a large purchase or transferring existing debt, prioritize 0% APR offers

- If paying in full: When never carrying a balance, focus on cash back rewards

- Hybrid needs: Some cards offer both solid cash back and introductory 0% periods

- Timeline consideration: Consider both immediate financing needs and long-term rewards potential

The interest savings from a 0% APR offer typically dwarf potential cash back if you’ll be carrying a significant balance. For example, $5,000 carried for 15 months at 18% APR would accumulate about $1,125 in interest—far more than typical rewards earnings on that spending.

“How many cash back cards is too many?”

There’s no universal answer, but consider these factors:

- Management capacity: How many cards can you realistically track without missing payments?

- Spending volume: Is your spending sufficient to justify multiple cards?

- Annual fee total: How much are you paying annually across all cards?

- Credit impact: How might multiple cards affect your credit profile?

Most people find 2-4 cards manageable without excessive effort. Beyond that, the incremental benefit often diminishes while complexity increases. Start conservatively and add cards only when you’re comfortable managing your existing portfolio.

The Bottom Line: Getting Cash Back Without the Headaches

Cash back credit cards offer a straightforward path to earning rewards on everyday spending. Unlike more complex travel rewards programs, cash back provides clear value with minimal learning curve and maximum flexibility in how you use your rewards.

The ideal cash back strategy varies significantly based on your spending patterns, organizational preferences, and whether you value simplicity or maximum returns. For many consumers, a combination of 2-3 carefully selected cash back cards provides the sweet spot—maximizing rewards across different spending categories without creating excessive complexity.

As you develop your cash back strategy, keep these core principles in mind:

- Pay balances in full to avoid interest charges that obliterate your rewards

- Choose cards that actually align with your real spending patterns, not theoretical ones

- Be strategic about category bonuses and spending caps

- Set up systems to ensure you’re using the right card for each purchase

- Regularly reassess your card portfolio as your spending habits evolve

With a thoughtful approach, cash back cards can provide a meaningful return on your everyday spending—putting hundreds or even thousands of dollars back in your pocket annually without requiring you to become a points and miles expert.

Disclaimer: Credit card terms, conditions, and offers change frequently. Information in this guide is accurate as of April 18, 2025. Always verify current offer details directly with card issuers before applying. This content is for informational purposes only and should not be considered financial advice.

AFFILIATE DISCLOSURE: CreditCardWisdom.com may receive compensation when visitors apply through our links and are approved. While we strive to provide comprehensive information about all available cards, our reviews feature cards from our partners. Our editorial integrity is not influenced by compensation arrangements, and we evaluate all cards using consistent standards. See our advertising policy for more details.