Metal Credit Cards Worth Having in 2025: Status Symbol or Practical Value?

A comprehensive review of luxury metal credit cards and whether they’re worth the hype

Picture this: You’re out for dinner with friends, the bill arrives, and you casually slide out your metal credit card. As it lands on the table with that distinctive “thunk,” a few heads turn. C’mon, we’ve all either done it or daydreamed about it! I’ll admit it – the first time I pulled out my metal card at a fancy restaurant, I may have placed it down a little more dramatically than necessary. Hey, no judgment here!

I’ve spent way too many hours (just ask my spouse!) obsessing over the latest metal credit cards, comparing their benefits, wincing at those hefty annual fees, and figuring out whether they actually deliver real value – or if they’re just glorified paperweights designed to make us feel fancy while we buy ordinary things like groceries and gas.

Whether you’re itching to upgrade your wallet game with something that makes a statement or you’re just wondering if these shiny rectangles are worth the fuss, I’ve got you covered. Let’s ditch the marketing fluff and get down to what really matters – will these cards actually improve your financial life, or are they just expensive toys for grown-ups?

The TL;DR Version:

Metal credit cards can be amazing – but only if you’ll actually use the perks they offer. Otherwise, you’re basically paying hundreds of dollars a year for the privilege of carrying around a slightly heavier rectangle in your wallet. Not exactly financial genius, right?

Friendly Affiliate Disclosure: I may earn a small commission if you apply for cards through links in this post. Don’t worry – it doesn’t cost you anything extra, and these commissions help keep the lights on around here! I only recommend cards I’ve thoroughly researched or personally used, and I’d suggest the same ones to my friends and family. Your support helps fund my late-night coffee habits while writing these reviews, and I’m genuinely grateful for it!

What’s In This Guide

- The Metal Card Fascination

- What Makes These Cards Special (Besides the Metal)

- My Top Metal Credit Card Picks for 2025

- Side-by-Side Comparison of 2025’s Metal Cards

- The Good, The Bad, and The Heavy: Pros and Cons

- Who Should (and Shouldn’t) Get a Metal Card

- The Big Question: Are Metal Cards Worth It in 2025?

- Your Burning Questions Answered

- Beyond the Bling: Final Thoughts

What Makes These Cards Special (Besides the Metal)

Let’s get into the nitty-gritty of what we’re actually talking about when we say “metal credit cards.” Unlike your run-of-the-mill plastic cards that bend at the slightest touch, these sturdy beauties are crafted from—surprise, surprise—actual metal! They typically feature:

- Stainless steel (the Toyota of metal cards—reliable and common)

- Titanium (the Tesla—lightweight but strong)

- Brass (the vintage car—classic and hefty)

- Copper (the hipster choice—unique and develops a patina)

- And for the “my wallet is heavier than yours” crowd, sometimes even precious metals like gold (looking at you, Luxury Card Mastercard® Gold Card)

These cards typically weigh between 12 to 22 grams, which might not sound like much until you compare them to regular plastic cards that weigh about 5 grams. That extra weight is what gives you that satisfying “I’ve clearly made excellent life choices” thunk when you drop it on a table. Some are solid metal throughout, while others are metal-plastic sandwiches (which sounds less appetizing than it is).

But let’s be real—we’re not just talking about fancy metal rectangles. These cards usually come with some serious perks:

- Higher annual fees that’ll make your grandma clutch her pearls ($95 to $695 is standard, with some invite-only cards soaring past $5,000)

- Rewards programs that actually make mathematical sense for big spenders

- Airport lounge access that’ll make you feel sorry for the folks sitting on the floor by the gate

- Concierge services for when you absolutely need dinner reservations at that impossible-to-book restaurant

- Statement credits that can actually make these cards “free” if you’re organized enough to use them

The whole metal card craze kicked off when American Express launched their mythical Centurion Card (aka “The Black Card”) back in 1999. It was the card you couldn’t apply for—it had to invite you. Fast forward to 2025, and metal cards have gone mainstream. These days, you don’t need to own a small country to get your hands on one—just decent credit and, for many of them, the willingness to shell out for an annual fee.

My Top Metal Credit Card Picks for 2025

Alright, now that we’ve covered the basics, let’s get to the good stuff! After spending an embarrassing amount of time analyzing these cards (seriously, my spreadsheet would make an accountant weep with joy), here are my top picks for 2025, categorized by what they do best:

Best Overall: Capital One Venture X Rewards Credit Card

Annual Fee: $395 (I know, I know—but stick with me here)

The Capital One Venture X has become the darling of the metal card world for good reason. At 17 grams, it’s substantial enough to make you feel fancy but won’t tear a hole in your pocket. What I love about this card is how it threads the needle between premium benefits and a reasonable(ish) annual fee.

The math is actually pretty simple: You get a $300 annual travel credit through Capital One Travel, plus 10,000 anniversary bonus miles (worth $100 in travel). Boom—that’s $400 in value right there, already offsetting the annual fee. Throw in airport lounge access including Capital One’s super sleek new lounges (the one in Dallas has shower suites nicer than my bathroom at home), and you’re golden.

Last month, I used mine for a trip to Chicago and earned 10x miles on the hotel, 5x on the flight, and 2x on everything else. The points accumulated so fast I could practically watch them grow!

Most Prestigious: The Platinum Card® from American Express

Annual Fee: $695 (yes, you read that right!)

If credit cards were high school students, the Amex Platinum would be the rich kid driving a BMW to school. Weighing in at a substantial 18.5 grams, it’s the heavyweight champion of widely available metal cards. When you pull this bad boy out, even seasoned waiters might raise an eyebrow.

That $695 annual fee made me choke on my coffee the first time I saw it, but here’s the thing—if you’re a frequent traveler who likes nice things, the math can actually work. With more airport lounge access options than any other card (I once spent a 4-hour layover hopping between lounges just because I could), plus annual credits for airlines, hotels, digital subscriptions, and even $100 to spend at Saks Fifth Avenue, the perks add up fast.

My brother-in-law is obsessed with his Platinum card and swears the Fine Hotels & Resorts program alone has scored him room upgrades, late checkouts, and free breakfasts worth way more than the annual fee. Must be nice!

Best Value: Chase Sapphire Preferred® Card

Annual Fee: $95 (practically a bargain in this crowd)

If the Venture X and Amex Platinum are making your wallet cry, the Chase Sapphire Preferred is here to dry its tears. At just $95 annually, it’s the Toyota Camry of metal cards—reliable, accessible, and secretly pretty awesome. At 12.4 grams, it’s lighter than some premium options but still has enough heft to make you feel like you’ve “made it” without actually having to make it all the way to the 1%.

I carried this card for three years before upgrading, and that 100,000-point welcome bonus (after meeting spending requirements) was enough to fund a round-trip flight to Europe. Not too shabby! Earning 5x points on travel booked through Chase, 3x on dining and groceries, and the 25% boost when redeeming for travel through Chase makes this card a sleeper hit.

Fun fact: When I first got this card, I definitely practiced that smooth card-flip move from casino movies before using it in public. Did I look cool? Absolutely not. Did my points still add up the same? You bet!

Best for Travelers: Chase Sapphire Reserve®

Annual Fee: $550 (gulp)

Ah, the legendary Chase Sapphire Reserve—the card that broke the internet back in 2016 when it launched. At 12.6 grams, it’s surprisingly not the heaviest card on this list, but what it lacks in weight, it makes up for in street cred among frequent travelers.

Here’s what I love about this card: That $550 annual fee looks scary until you realize the $300 annual travel credit is basically automatic for anyone who, you know, travels. That brings the real cost down to $250, and then the 50% boost when redeeming points for travel through Chase is where the magic happens.

My cousin is a consultant who practically lives in airports, and she once told me, “This card pays me to have it, not the other way around.” Between the 10x points on hotels and car rentals (after the travel credit), 5x on flights, and 3x on other travel and dining, she earns enough points each year to take her family on a luxury vacation. Last summer they flew business class to Japan, and I’m still trying not to be envious!

Best for Foodies: American Express® Gold Card

Annual Fee: $325 (up from $250, much to everyone’s dismay)

I have a friend who calls her Rose Gold Amex “the foodie flexer” – and she’s not wrong! The 14.7-gram Amex Gold has seen its annual fee creep up to $325 in 2025, but if you’re the kind of person who can identify restaurants on Instagram just by the plating, this might still be your perfect match.

With 4x points at restaurants worldwide and U.S. supermarkets (up to $25,000/year), this card turns your food obsession into travel opportunities. The new benefits are giving me mixed feelings—monthly credits for Dunkin’ are great if you’re a coffee addict like me (guilty as charged), but the semi-annual Resy credits feel a bit niche.

I watched my sister-in-law tally up her credits from this card last Christmas, and between the Uber Cash, dining credits, and Dunkin’ visits, she’d offset almost the entire annual fee without changing her normal spending habits. “I’d be buying these lattes anyway,” she shrugged, “might as well get them for free.”

Best No Annual Fee: Bilt World Elite Mastercard®

Annual Fee: $0 (you read that right—zero, zilch, nada!)

Wait, a metal card with NO annual fee? That’s like finding a unicorn that also does your taxes! The Bilt Mastercard is truly a game-changer, especially if you’re a renter who feels the sting of writing that giant check each month without earning any rewards.

Let me tell you about my neighbor who recently got this card—she pays $2,400 in rent monthly (welcome to city living), and now earns points on what was previously just money out the door. With 1x points on rent payments with no fees (up to 100,000 points annually), plus 3x on dining, 2x on travel, and 1x on everything else, she’s on track to earn enough points for a weekend getaway after just a few months.

Oh, and did I mention this card is FREE? As in, you get the satisfying weight and clunk of metal without paying any annual tribute to the credit card gods. For renters especially, this card is like finding money in your coat pocket—a delightful surprise in a world of expensive metal cards.

Side-by-Side Comparison of 2025’s Metal Cards

I’ve spent countless hours comparing these cards (my spouse now refers to my spreadsheets as “the other relationship”), so you don’t have to! Here’s how they stack up against each other:

Quick Affiliate Reminder: If you click through and apply for any of these cards, I might earn a small commission (think coffee money, not yacht money). This doesn’t influence which cards make my list or how I rank them—I’d recommend these same cards to my mom! Your support through these links helps keep this site running without those annoying popup ads we all hate.

| Card | Annual Fee | Weight | Welcome Bonus | Key Rewards | Notable Benefits |

|---|---|---|---|---|---|

| Capital One Venture X | $395 | 17g | 75,000 miles after spending $4,000 in 3 months | 10x on hotels/rentals via Capital One Travel, 5x on flights, 2x on everything else | $300 travel credit, lounge access, 10,000 anniversary miles, cell phone protection |

| Amex Platinum | $695 | 18.5g | 80,000 points after spending $6,000 in 6 months | 5x on flights booked directly or through Amex Travel, 5x on prepaid hotels through Amex Travel | $200 airline fee credit, $200 hotel credit, extensive lounge access, Uber credits, Saks credits |

| Chase Sapphire Preferred | $95 | 12.4g | 100,000 points after spending $4,000 in 3 months | 5x on travel through Chase, 3x on dining, select streaming services, online groceries, 2x on other travel | 25% boost on travel redemptions, annual $50 hotel credit, primary rental car insurance |

| Chase Sapphire Reserve | $550 | 12.6g | 60,000 points after spending $4,000 in 3 months | 10x on hotels/car rentals through Chase (after $300 travel credit), 5x on flights, 3x on other travel/dining | $300 travel credit, Priority Pass lounge access, 50% boost on travel redemptions |

| American Express Gold | $325 | 14.7g | 60,000 points after spending $4,000 in 6 months | 4x at restaurants worldwide, 4x at U.S. supermarkets (up to $25,000/year), 3x on flights | $120 dining credit, $120 Uber cash, $120 Dunkin’ credits, $100 Resy credit |

| Bilt World Elite Mastercard | $0 | 13g | None | 3x on dining, 2x on travel, 1x on rent (no fees) and other purchases | No fees on rent payments, points transfer to travel partners, cell phone protection |

| Citi / AAdvantage Executive | $595 | 18g | 50,000 miles after spending $5,000 in 3 months | 4x on eligible American Airlines purchases, 2x on restaurants and gas stations, 1x on everything else | Admirals Club access for you and 8 guests, first checked bag free, priority boarding |

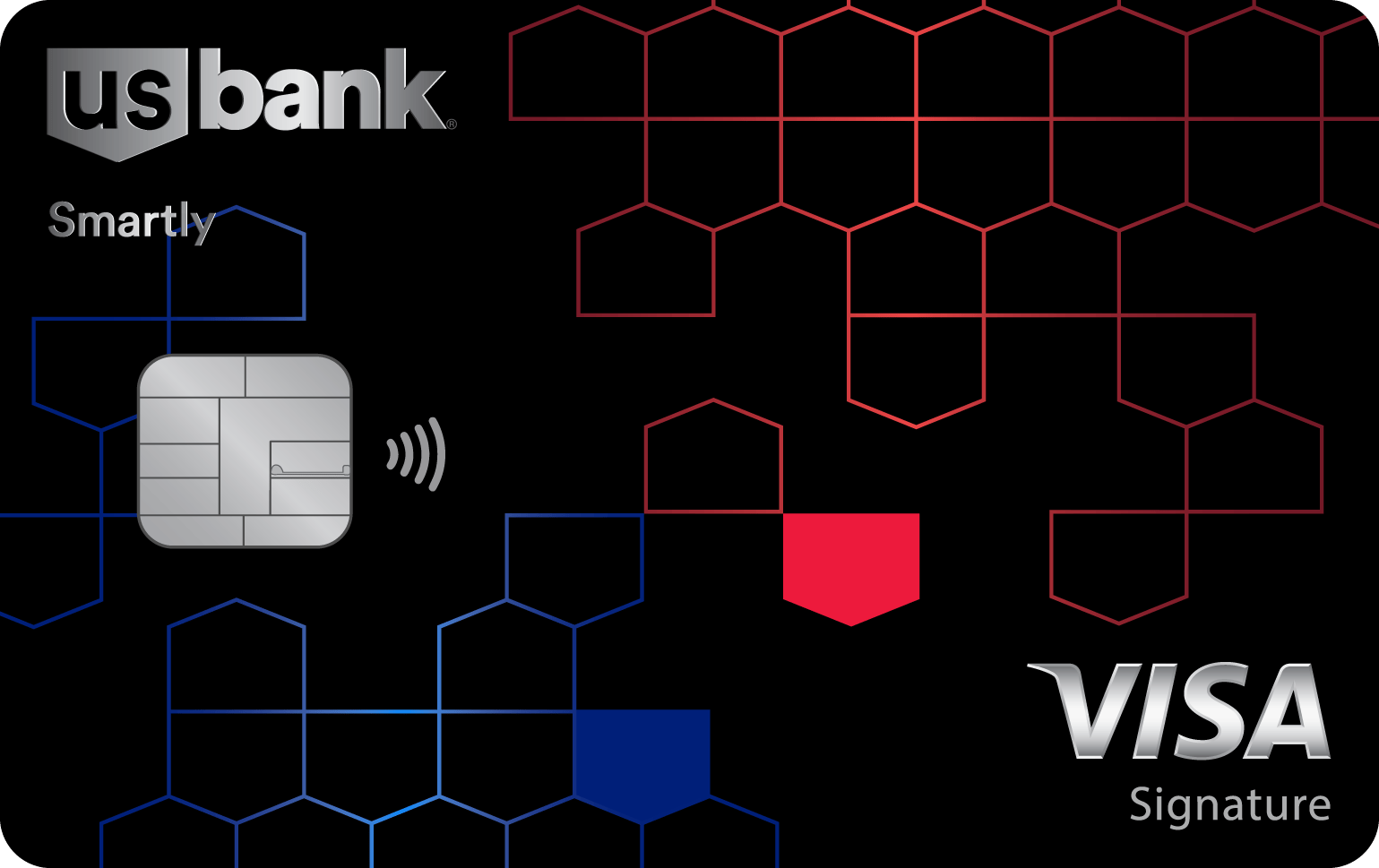

| U.S. Bank Altitude Reserve | $400 | 13g | 50,000 points after spending $4,500 in 90 days | 5x on prepaid hotels/car rentals through U.S. Bank’s travel portal, 3x on travel, mobile wallet purchases | $325 travel/dining credit, 30% in-flight WiFi discount, Priority Pass lounge access |

The Good, The Bad, and The Heavy: Pros and Cons

Let’s get real for a minute—metal credit cards look cool and feel amazing, but are they actually worth it? After carrying several of these cards over the years, here’s my unfiltered breakdown of the good and the not-so-good:

The Awesome Stuff

They’re Basically Indestructible

Remember that plastic card that went through the washing machine and came out curled like a taco? Yeah, that doesn’t happen with metal cards. They laugh in the face of washing machines, survive being sat on, and keep their numbers pristine for years. My oldest metal card still looks brand new after four years of heavy use.

Premium Perks That Actually Matter

Most (but not all) metal cards come with benefits that can genuinely improve your travel experience. The first time I breezed past the general boarding line, got free checked bags, and relaxed in an airport lounge with complimentary food and drinks, I thought, “OK, now I get it.” These perks can transform travel from stressful to enjoyable.

Slightly Better for Mother Earth

Since metal cards last longer, you’ll need fewer replacements over time. Given how many plastic cards end up in landfills, this is a small but real environmental win. I’ve replaced plastic cards almost yearly, while my metal cards just keep going.

The Conversation Factor

I hate admitting this, but people notice metal cards. They’ve sparked conversations in checkout lines, at restaurants, and even led to a job connection once when a hiring manager noticed my card. Is this a reason to get one? Probably not. Is it a fun side effect? Absolutely.

Better Treatment (Sometimes)

I’ve personally experienced better service at high-end hotels and restaurants when using certain metal cards. It’s not guaranteed, but there have been times when a room upgrade or better table mysteriously appeared after I presented my metal card. Coincidence? Maybe, but it’s happened too often to ignore.

The Not-So-Great Stuff

Those Eye-Watering Annual Fees

Let’s not sugarcoat it—most metal cards charge fees that would make your grandmother faint. From $95 on the low end to $695 (or more) on the high end, these aren’t small expenses. If you don’t use the benefits enough to offset these fees, you’re basically paying hundreds of dollars for a shiny rectangle. Not exactly financial genius!

Your Wallet Might Need a Chiropractor

These cards are heavier than their plastic counterparts—which feels cool until you’re carrying three or four of them. My wallet gained almost 40 grams when I switched to primarily metal cards, and yes, I actually noticed the difference. They can also set off metal detectors at security checkpoints, which is always a fun explanation…

The Breakup is Complicated

When you’re done with a plastic card, you cut it up and toss it. With metal cards? Good luck! Most require you to mail them back to the issuer in special envelopes. I once tried to cut one with regular scissors and nearly injured myself while the card remained smugly intact.

They’re Not Special Anymore

In 2015, a metal card was a head-turner. In 2025? They’re everywhere. The exclusivity factor has definitely diminished as more issuers offer metal options. My barista now has the same card I felt so special about getting a few years ago.

Contactless Can Be Wonky

Some metal cards struggle with contactless payment technology because, well, metal blocks signals. This has improved with newer card designs, but I’ve definitely experienced the embarrassing “tap, tap… sorry let me insert it instead” moment more often with metal cards than plastic ones.

Who Should (and Shouldn’t) Get a Metal Credit Card in 2025?

Let’s be brutally honest—metal credit cards aren’t for everyone. Like that fancy espresso machine that seemed like a good idea but now collects dust in your cabinet, these cards can be amazing for some people and a waste of money for others. Here’s my take on who should reach for metal and who should stick with plastic:

Metal Cards Are Great For…

Road Warriors and Frequent Flyers

If your carry-on has more miles than your car, these cards make total sense. When you’re constantly traveling, perks like lounge access, trip insurance, and free checked bags go from “nice to have” to “essential for sanity.” One delayed flight with lounge access can make a $550 annual fee feel completely justified.

Big-Time Spenders

If you’re putting $50K+ annually on credit cards (whether for personal or business reasons), the enhanced earning rates on premium categories can rack up serious rewards. My friend who runs a small business puts all his expenses on his Amex Platinum and takes his family on essentially free vacations every year just from the points.

The Super-Organized Benefit Maximizers

You know who you are—you’ve got alerts set for every monthly credit, you track your points in a spreadsheet, and you know exactly which card to use for which purchase. If that sounds like you, you’ll likely extract every penny of value from these cards and then some.

Those in Image-Conscious Industries

Let’s face it—in some fields, appearance matters. If you’re in finance, real estate, law, or entertainment where client perception is important, the subtle statement of a premium card might actually provide tangible business value. I’ve literally seen business deals discussed over which metal card someone carries (weird but true).

Probably Not Worth It For…

Occasional Card Users

If you only pull out your credit card for the occasional big purchase or emergency, the math simply won’t work. I have a friend who pays for almost everything with cash or debit, got a premium card for the “perks,” and then realized she’d spent $550 to earn about $75 worth of points. Ouch!

Anyone Carrying a Balance

I cannot emphasize this enough—if you’re currently paying interest on credit card debt, please focus on paying that down instead of adding a fancy new card to your wallet. The 18%+ interest you’re paying will obliterate any benefits these cards provide. Fix your debt first, then consider premium cards.

The “I’ll Get To It Later” Crowd

Be honest with yourself—if you know deep down that you’ll never remember to use the monthly Uber credits, won’t bother activating the benefits, and will forget about the annual travel credit, these cards will end up being very expensive paperweights. Premium cards reward organization and intentionality.

Dedicated Minimalists

If you’re someone who values simplicity above all else, the complex benefits structures of these cards will feel like mental clutter rather than value. There’s something to be said for having one simple card with straightforward rewards and no annual fee to track or benefits to maximize.

Here’s the honest truth: a credit card is only “worth it” if it fits YOUR specific life and spending patterns. The card that’s perfect for your jet-setting friend might be a complete waste of money for you. And that’s totally okay! Financial decisions shouldn’t be based on what looks cool—they should be based on what actually works for your unique situation.

The Big Question: Are Metal Cards Worth It in 2025?

After spending years with various metal cards in my wallet (and several hundred dollars in annual fees later), I’ve reached a conclusion that might frustrate you: metal credit cards can be absolutely worth it… for some people, in some situations, sometimes.

I know, I know—not exactly the clear-cut answer you were hoping for! But let me break it down in a way that might actually help you decide:

Let’s Talk About the Status Thing

Can we just acknowledge the elephant in the room? Yes, metal cards still carry some prestige in 2025, but WAY less than they did a few years ago. When my 22-year-old nephew got a metal card right out of college, I knew the exclusivity factor had definitely diminished.

If you’re secretly hoping your metal card will make people think you’re wealthier or more successful, I hate to break it to you, but that ship has pretty much sailed. In financial circles especially, people know that having a particular card says basically nothing about your actual financial situation. I’ve met millionaires with basic no-annual-fee cards and people barely making rent with premium metal cards.

The Real Value Calculation

Here’s where metal cards can truly shine—in their actual, tangible benefits, IF you use them. I’ve developed a simple formula that helps determine whether a card makes financial sense:

- Add up the REALISTIC value of benefits you’ll actually use. Be brutally honest here! If you know deep down you’ll probably only visit an airport lounge once a year, don’t pretend you’ll go monthly. If you’re likely to forget about statement credits, don’t count them.

- Calculate what you’d ACTUALLY earn in rewards. Look at last year’s spending as a guide and figure out what you would have earned with this card versus a good no-annual-fee option.

- Subtract the annual fee from your total. This number—positive or negative—is your personal “card value equation.”

- Don’t forget the intangibles. Some benefits like travel insurance or extended warranty are harder to value but can save thousands if you need them. My friend’s trip cancellation insurance covered a $4,200 non-refundable vacation when her mom got sick—instantly justifying several years of annual fees.

For me, the Capital One Venture X math works out beautifully—between the $300 travel credit, 10,000 anniversary miles, and higher earning rates, I come out about $300 ahead each year. But when I ran the same calculation for the Amex Platinum, I realized I wasn’t using enough of the benefits to offset that mammoth $695 fee, so I didn’t apply.

The Bottom Line (Finally!)

Based on my experience and obsessive research, metal credit cards are worth it when:

- You travel frequently enough to actually use those fancy perks (be honest with yourself here!)

- Your spending naturally aligns with the card’s bonus categories (don’t change your spending habits to fit a card)

- You’re organized enough to remember and use statement credits and benefits (set those calendar reminders!)

- Your math shows the value exceeds the annual fee by at least $100 (to account for overestimation)

They’re definitely NOT worth it when:

- You’re mainly attracted to the “cool factor” or status aspect (the novelty wears off FAST)

- You rarely travel or won’t use travel-focused benefits (lounge access isn’t worth much if you never visit lounges)

- You tend to forget about expiring credits and benefits (I know I’ve lost hundreds in unused credits)

- You’re carrying high-interest credit card debt (seriously, tackle that first!)

Remember, the truly “best” card isn’t the one with the most prestige or even the most benefits—it’s the one that aligns perfectly with YOUR specific life, spending habits, and organizational style. Sometimes that’s a fancy metal card, and sometimes it’s a simple no-annual-fee option.

Your Burning Questions Answered

After writing about metal credit cards for years, I’ve heard just about every question imaginable. Here are the ones that pop up most frequently:

The J.P. Morgan Reserve Card is the heavyweight champion at approximately 27 grams, but unless you’re managing millions with J.P. Morgan, good luck getting an invitation! For us mere mortals, the American Express Platinum (18.5 grams) and the Citi / AAdvantage Executive (18 grams) are among the heaviest commonly available cards. Yes, I’ve actually weighed them on a kitchen scale—my family thinks I’m bizarre.

Yes! The unicorn of the metal card world is the Bilt World Elite Mastercard—fully metal with a $0 annual fee. It’s especially valuable for renters. The Amazon Prime Visa is also metal with no annual fee, though you need an Amazon Prime membership ($139/year) to qualify. The Apple Card is another metal option with no annual fee, and while its rewards aren’t spectacular, it looks slick and integrates beautifully with the Apple ecosystem. I dropped mine in front of my tech-obsessed brother-in-law just to watch him drool over the titanium design.

Don’t try to destroy it yourself! Trust me on this—I once nearly stabbed myself trying to punch holes in an expired metal card. Most issuers now provide a prepaid return envelope when they send your replacement card. Just pop your old card in there and send it back for secure destruction. No envelope? Call your issuer and request one, or visit a local branch if that’s an option. Some people have told me they keep their expired metal cards as souvenirs, which seems both unnecessary and slightly concerning from a security perspective.

It might! Modern metal cards are designed to minimize this risk, but some of the heavier cards can indeed trigger metal detectors. I learned this the embarrassing way at airport security when my wallet set off the alarm. Pro tip: just put your wallet in the bin with your phone and keys when going through security. Otherwise, you might end up getting the pat-down while explaining to a stern TSA agent that yes, your credit card really is made of metal and no, you’re not carrying concealed weapons.

For most premium metal cards, you’re looking at needing a good to excellent credit score—typically 700+ to be competitive, and 740+ for the best approval odds on cards like the Amex Platinum. That said, some metal cards like the Amazon Prime Visa might be accessible with scores in the high 600s. Your income and relationship with the issuer also matter a lot. My friend with a “merely good” credit score but a long history with Chase got approved for the Sapphire Preferred when others with similar scores were denied. It’s always worth checking for pre-qualification options before applying to avoid unnecessary hard inquiries.

Most modern metal cards do support contactless payments, though the technology has had to be specially adapted to work through metal. In the early days of metal cards, contactless was often problematic, but card issuers have largely solved this by 2025, typically by incorporating non-metal segments or using hybrid construction techniques. That said, I’ve found that some thicker metal cards still occasionally struggle with tap-to-pay terminals, especially older ones. My Venture X works flawlessly with contactless, while my older metal card sometimes requires the “tap, tap again harder, sigh dramatically, just insert it” routine that we all know and love.

Generally speaking, metal cards work exactly the same as plastic ones at the vast majority of merchants. They operate on the same payment networks (Visa, Mastercard, American Express, etc.) and are accepted anywhere those networks are. The only issues I’ve occasionally encountered are with certain older automated payment machines that weren’t designed with thicker cards in mind—like some parking meters and older vending machines. And of course, American Express cards (metal or otherwise) are still less widely accepted than Visa or Mastercard, especially internationally. I learned this the hard way in a tiny restaurant in rural Italy when my Amex was politely declined and I had to wash dishes… just kidding, I had a backup Visa.

Usually not. The metal construction is typically specific to certain card products, and issuers don’t generally offer metal versions of cards designed to be plastic. That said, you might be able to upgrade your account to a premium version that happens to come in metal, assuming you qualify. For example, you can’t get a metal version of a basic Chase Freedom card, but you might be able to upgrade it to a Sapphire Preferred, which is metal. Some issuers like American Express occasionally offer targeted upgrade opportunities from plastic to metal cards. I was once offered an upgrade from my everyday Amex to the Gold card with a reduced first-year annual fee—naturally, I jumped at it, partly for the better rewards and partly because, well, shiny!

One Last Affiliate Mention: Some of the card offers appearing in this review come from companies that compensate me when you’re approved. This might affect which cards appear here, but it NEVER affects my opinions or how I rank them. I’ve actually turned down partnerships with cards I don’t believe in, even when they offered higher commissions. My recommendations are based on what I’d genuinely suggest to my friends and family—because maintaining your trust is worth way more than a few extra commission dollars!

Beyond the Bling: Final Thoughts

After spending years obsessing over, researching, and personally carrying various metal credit cards (my wallet has literally gotten heavier!), I’ve come to appreciate both their genuine benefits and their limitations. These days, metal cards offer a mix of actual value and aesthetic appeal—but they’re no longer the exclusive status symbols they once were.

The truth is, substance should always win over style when it comes to financial tools. A gorgeous metal card that costs you more in annual fees than you get back in benefits is basically an expensive fashion accessory. It’s like buying designer shoes that hurt your feet—they might look fabulous, but you’ll regret the purchase every time you use them.

If you’re thinking about adding a metal card to your wallet, start with an honest self-assessment. Will you actually use those airport lounges, or do you arrive at the gate five minutes before boarding? Will you remember to claim all those monthly credits, or will they expire unused? Do you spend enough in the bonus categories to earn meaningful rewards? Your answers should guide your decision far more than how cool the card looks when you casually toss it onto a restaurant table (though I totally understand the appeal of that satisfying “thunk”).

For 2025, I think the Capital One Venture X offers the best overall value for most people seeking a premium metal card experience. It hits that sweet spot between meaningful benefits and manageable cost. The Chase Sapphire Preferred remains the best entry point if you’re curious about metal cards but not ready for a three-digit annual fee, while the Amex Platinum continues to shine for frequent travelers who can maximize its extensive perks.

Ultimately, remember that credit cards—metal or otherwise—are tools to help you reach your financial goals, not status symbols or accessories. Choose wisely, use responsibly, and never, ever carry a balance if you can avoid it. The true measure of financial success isn’t the weight of the cards in your wallet but the wisdom of the decisions you make with them!

A Little Personal Confession:

I’ll admit it—I totally got my first metal card partly because it looked and felt cool. And yes, there was a period where I may have deliberately set it down a little harder than necessary when paying for dinner. But you know what? The cards I’ve kept long-term aren’t the ones that impressed my friends—they’re the ones that consistently save me money and enhance my travel experiences.

The excitement of metal wears off surprisingly quickly (trust me on this), but the value of well-chosen benefits compounds over time. So choose substance over style, and you’ll build actual wealth instead of just the appearance of it. And isn’t that the whole point?